In various specialized industries such as construction, telecommunications, and forestry, the use of outsourced labor is inevitable. Outsourced labor plays a crucial role in the operation and development of businesses. Accounting for outsourced labor costs can sometimes be challenging, especially when determining corporate income tax (CIT). MPBPO understands that managing outsourced labor costs requires precision and careful calculation. We will work alongside businesses to find optimal solutions so that outsourced labor costs are accounted for reasonably, maximizing the benefits for the company in determining taxes and managing finances.

>>> See more: What is Outsourcing?

Outsourced Labor Costs and Applicable Legal Basis

Outsourced labor costs are a significant part of production and management expenses for businesses. When hiring external labor, companies not only have to pay wages to the workers but also face many related costs. These costs may include:

Outsourced Labor Costs

First of all, to successfully negotiate with laborers, we need to clearly understand the concept of this type of labor. Hiring labor is not just about utilizing human labor to perform tasks according to requirements; it also involves a range of incurred costs. Outsourced labor costs can be understood as the total amount a business must pay after these workers have completed the work according to the agreed contracts. This includes basic costs such as wages and other payments like social insurance, health insurance, and allowances.

Businesses have several options when deciding to hire external labor. One option is to contract workers individually, leveraging the professionalism and availability of those specialized in a particular job. Another option is to contract workers through business entities, expanding the search for high-quality personnel. Moreover, businesses can hire construction contractors to ensure the quality and progress of a project. This not only reduces management pressure but also ensures professionalism and efficiency in the project’s execution. Alternatively, companies can find workers themselves, meaning they hire directly from the labor market. While this requires more effort in selection and management, it offers greater flexibility and control over internal labor processes.

Applicable Legal Basis

Summarizing and managing outsourced labor costs has become one of the major challenges in construction accounting. Accountants need to continuously track and record the expenses of a large number of workers throughout various stages of the construction project. Fortunately, this task has become easier with the support of construction accounting software.

Faced with numerous legal factors, construction accountants must comply with several legal documents and regulations. Legal information and documents regarding outsourced labor costs include:

- Circular 92/TT-BTC dated June 15, 2016, guiding personal income tax and value-added tax obligations for resident individuals engaged in business activities.

- Clause 1, Article 6 of Circular 78/2014/TT-BTC dated March 31, 2014, providing for deductible expenses.

- Point a, Clause 2, Article 2 of Circular 111/2013/TT-BTC dated August 15, 2013, on income from wages and salaries.

- Point i, Clause 1, Article 25 of Circular 111/2013/TT-BTC dated August 15, 2013, on personal income tax withholding.

Additionally, regulations from the 2014 Social Insurance Law and the 2019 Labor Law also play a crucial role in determining and applying costs related to labor.

Understanding these regulations helps businesses establish a flexible and efficient accounting system while ensuring full compliance with legal requirements, minimizing legal risks, and optimizing labor costs.

Documentation and Methods for Accounting for Outsourced Labor Costs

Accounting for outsourced labor costs requires diligence and accuracy from businesses. To ensure a smooth accounting process that complies with legal regulations, preparing complete documents and records is essential.

Case 1: The company outsources labor to an individual not engaged in business

In the case where a company outsources labor to an individual not engaged in business, accounting for labor outsourcing costs requires precision and compliance with tax regulations. Below is the detailed accounting method:

- Recording costs:

- Debit Account: 627/622 (Labor costs for outsourced services)

- Credit Account: 331 (Payable to labor).

- Withholding 10% personal income tax (PIT):

- Debit Account: 331 (Payable to labor)

- Credit Account: 3335 (Withheld personal income tax).

- Upon payment:

- Debit Account: 331 (Payable to labor)

- Credit Account: 111,112 (Cash or Bank).

At the same time, the company must pay attention to some important points in preparing the documents:

- Outsourcing contract: The contract should be fully and clearly prepared, especially regarding working conditions, wages, and tax obligations.

- Acceptance report and confirmation of outsourced work volume: These are essential documents to confirm that the worker has completed the job as required and serve as a basis for payment.

- Identity cards and payment documents: It is necessary to have the identity card of the representative and each worker in the team, along with cash or bank payment receipts to prove wage payment.

- Personal income tax withholding documents: These documents serve as evidence that the company has made the required personal income tax withholdings according to regulations.

Case 2: The company outsources labor to an individual engaged in business

In the case where the company outsources labor to an individual engaged in business, the accounting process for outsourced labor costs also requires accuracy and adherence to tax regulations. Below is the detailed accounting method:

- Recording costs:

- Debit Account 627/622 (Labor costs for outsourced services)

- Credit Account 331 (Payable to labor).

- Upon payment:

- Debit Account 331 (Payable to labor)

- Credit Account 111,112 (Cash or Bank).

- For invoices: For labor payments exceeding VND 100 million per year, a separate invoice must be issued and maintained. If the labor payment is less than VND 100 million per year, an invoice is not required, but other documents proving payment must still be maintained.

Documents include:

- Outsourcing labor contract: The contract should be fully prepared with terms related to work, wages, and tax obligations.

- Acceptance report and settlement of outsourced work volume: These documents serve as the basis for confirming and paying labor costs, and they must be carefully maintained.

- Labor invoice: If the labor payment from the business individual meets the required threshold, the labor invoice must be preserved to ensure legality and compliance with regulations.

The accounting process and document preservation should be conducted meticulously to avoid tax and legal risks during tax finalization and inspections by tax authorities.

Case 3: The company hires a construction contractor

In the case where the company hires a construction contractor, the accounting process for outsourced labor costs also requires precision and vigilance regarding any risks that may arise. Below is the detailed accounting method:

- Recording costs:

- Debit Account 627/622 (Labor costs – Outsourced services)

- Credit Account 331 (Payable to labor).

- Upon payment:

- Debit Account 331 (Payable to labor)

- Credit Account 111,112 (Cash or Bank).

Document notes:

- Outsourced labor contract: The contract should clearly outline the terms related to labor, project scope, and commitments to work quality.

- Acceptance report and confirmation of outsourced work volume: Accurate records of the progress and work volume completed must be maintained to support payments.

- Final settlement of outsourced work volume: This is the final step of the process, ensuring that the settlement is thoroughly conducted and accepted by both parties.

- VAT invoice: For construction services, the VAT invoice is an important part of the documentation to ensure compliance with tax regulations.

- Immediate payment orders: If applicable, the documentation should include immediate payment orders to prove authorization and acceptance of payment.

Important note: Before collaborating, the company should thoroughly check the contractor to avoid risks related to invoices, debts, and tax evasion.

Case 4: The company hires labor directly

In the case where the company hires labor directly, the accounting process for outsourced labor costs also requires precision and compliance with tax regulations. Below is the detailed accounting method for both cases: signing a labor contract for less than one month and for one month or more.

Hiring labor for less than one month:

-

Recording costs:

-

Debit Account 622 (Labor costs – Services)

-

Credit Account 334 (Payable to labor).

-

- Withholding 10% PIT (if applicable):

-

Debit Account 334 (Payable to labor)

-

Credit Account 3335 (Withheld PIT).

-

-

Upon payment:

-

Debit Account 334 (Payable to labor)

-

Credit Account 111,112 (Cash or Bank).

-

Hiring labor for one month or more:

-

Recording costs:

-

Debit Account 622 (Labor costs – Services)

-

Credit Account 334 (Payable to labor).

-

-

Social insurance deductions: If the contract is for one month or more, social insurance should be deducted from labor costs.

-

Debit Account 622,334 (Labor costs – Services)

-

Credit Account 338 (Payable to Social Insurance).

-

-

Withholding 10% PIT (if applicable):

-

Debit Account 334 (Payable to labor)

-

Credit Account 3335 (Withheld PIT).

-

-

Upon payment:

-

Debit Account 334 (Payable to labor)

-

Credit Account 111,112 (Cash or Bank).

-

Note: For cases involving PIT withholding, the company must properly apply Form 02/CK-TNCN to temporarily avoid withholding 10% PIT.

All documents such as contracts, timesheets, commitment forms, and payment receipts should be carefully preserved to ensure accuracy and legal compliance.

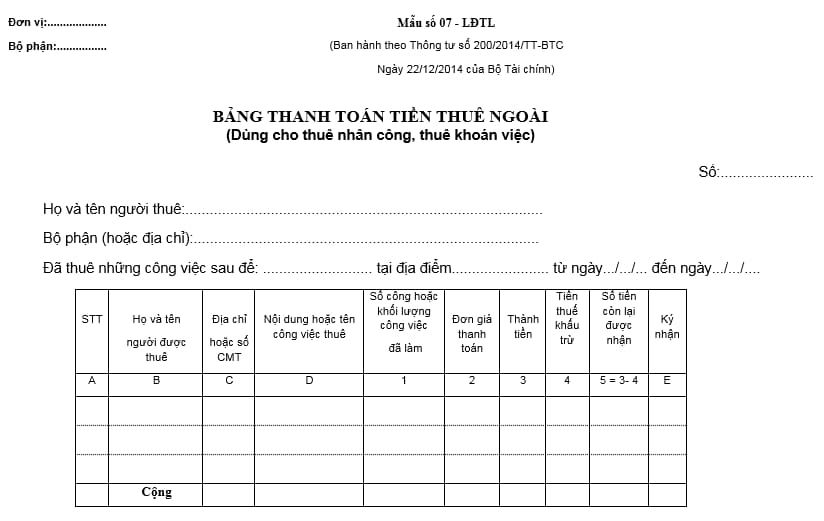

Template for Accounting Outsourced Labor Costs

The outsourced labor cost template plays an important role in managing and confirming the amount paid to external labor. Alongside the accounting methods for labor costs that have been presented earlier, using this template offers many benefits and convenience.

Here are some sample outsourced labor cost templates you can refer to:

Solution to Reduce Labor Costs through Outsourced Labor Services

MPBPO is a reliable partner in the field of Business Process Outsourcing (BPO), proud to provide services with a top-quality workforce. We are not just service providers but strategic partners, supporting customers in maximizing their business efficiency. At MPBPO, we focus on optimizing every business process of our clients, not just simply outsourcing personnel. Our team is not only highly skilled but also flexible and creative, ready to meet all challenges and offer smart solutions. We understand that each business has its own unique characteristics and requires personalized solutions. This drives us to continuously strive to ensure that every BPO solution is specifically designed to meet the strategic needs and objectives of each partner. For MPBPO, the success of our clients is also our success.

>>> See more: HR Outsourcing Services

Conclusion

Outsourced labor is increasingly becoming a pillar in the development strategy of businesses. By utilizing this service, they not only save time and management resources but also focus strongly on core development values.

In the future, outsourced labor will continue to thrive, driving economic growth with a flexible working model. To achieve high efficiency, organizations need to look further and integrate information from new technology trends, such as artificial intelligence. This helps the selection and management of personnel to become stronger, creating a dynamic working environment while also reducing costs effectively.

BPO.MP COMPANY LIMITED

– Da Nang: No. 252, 30/4 St., Hoa Cuong Bac ward, Hai Chau district, Da Nang city

– Hanoi: 10th floor, SUDICO building, Me Tri street, Nam Tu Liem district, Hanoi

– Ho Chi Minh City: 36-38A Tran Van Du, Tan Binh, Ho Chi Minh City

– Hotline: 0931 939 453

– Email: info@mpbpo.com.vn